PureFi — one-stop

compliance protocol

for decentralized finances

By AMLBot in partnership with Hacken

Abstract

PureFi is the only DeFi AML protocol for cryptocurrency onboarding. Developed by AMLBot in partnership with Hacken Foundation it aims to provide a full-cycle solution for cryptoasset analytics and AML/KYC procedures on the DeFi market. PureFi within a set of smart contracts will connect KYC/AML providers with DeFi users and Dexs/Defi projects in order to provide cryptoassets analytics and protect honest DeFi market players from “dirty money” risks. For example the liquidity pool user will be able to avoid the risk of getting an illegal money trail using the Verifiable Credentials certificate with his full-fledged AML/KYC data.

PureFi will be a cross-chain protocol based on the latest industry standards for Ethereum, BSC, Polkadot, Cosmos, and Casper Labs. Moreover, PureFi would not use information from one KYC/AML data provider, instead, we will be an open market for verified providers delivering ML analysis to DeFi market players.

We are looking forward to becoming the only platform that provides honest DeFi market players with ML risk protection and lets the users stay anonymous no matter what.

Introduction

Decentralized Finance (DeFi) has become more and more popular in the past few months. DeFi refers to all financial technologies that use blockchains and cryptocurrencies with the same aim in mind: to make cryptocurrency decentralized and independent from regulation by any financial agencies.

Decentralized Exchanges (DEXs), yield farming, stablecoins, lending platforms, wrapped coins and prediction markets are the most popular DeFi projects. The Ethereum blockchain serves as the base for the majority of applications.

DEX (decentralized exchange) is a blockchain-based peer-to-peer (P2P) online service that allows users to make direct cryptocurrency transactions between each other. DEXs don’t require users to pass know-your-customer (KYC) and are not custodian entities, unlike centralized exchanges. DEXs only provides the protocol that enables transactions. To be clear, users can easily create wallets and start trading without disclosing personal data.

According to the statistics, by Q1 '21 the overall monthly trade volume has almost tripled compared to the one as of December 2020 ($25 billion). The average daily DEX trade volume grew from $0.71 billion to $2.26 billion — a quarterly rise of 318%. Uniswap, the most popular DEX at the moment, had more volume than Coinbase, the most credible Centralized Exchange of the whole cryptomarket.

All that’s happening put DeFi under the radar of regulators and governments. Since most DeFi platforms ignore Know-Your-Customer (KYC) or Anti-Money Laundering (AML) procedures, they begin to foresee such transactions as a new haven for illegal activities.

In this context, the FATF declares to the G20 that jurisdictions must update requirements in order to implement AML/CFT mitigating measures. Furthermore, a new draft of the European Commission MiCa could restrict EU citizens from accessing DeFi projects. At least if they do not agree with the proposed strict legal regulations.

The problem

Since the fast growth of DeFi and DEXs has triggered huge attention in terms of Money Laundering and Terrorist Financing (ML/TF) risks, the lack of KYC and AML procedures became a crucial problem.

This is easily explained by the following significant factors:

- DEXs are based on blockchains, so they do not rely on specific jurisdictions or regulations;

- DEXs do not have access to users’ assets and are not performing AML/KYC verification on them;

- DEXs are in a grey area legally; some people contend that the DEXs are decentralized and therefore can not be governed, while others argue for a strictly defined legal system.

The statistics demonstrate that money laundering via DeFi is increasing - about $34 million of DeFi transactions in 2020 were conducted by criminal actors. Chainalysis forecasts and predicts exponential growth of illegal activity on the DeFi market and this causes another huge market problem - DEXs are regarded as dangerous by institutional investors and credible financial players around the world.

Beneficiaries

Liquidity pool users (liquidity providers)

Users supply their liquidity to the pool and when they withdraw their funds back, they automatically face the risk of getting "dirty" assets from illegal market players who use this opportunity to launder money.

Liquidity pools operators

Liquidity pool operators are interested in protecting themselves (and their users) from “dirty” funds. Some of them want their products to be more credible and adapt to comply with money laundering and governmental KYC regulation. As well, liquidity pool operators (especially who operate in regulated areas) are interested in working with verified counterparties and traditional financial organizations and yet being fully decentralized.

The solution

PureFi protocol provides the analysis of crypto wallets and transactions via AML databases in a form of Certificates based on the Verifiable Credentials standard - a machine readable by-default presentation of the data.

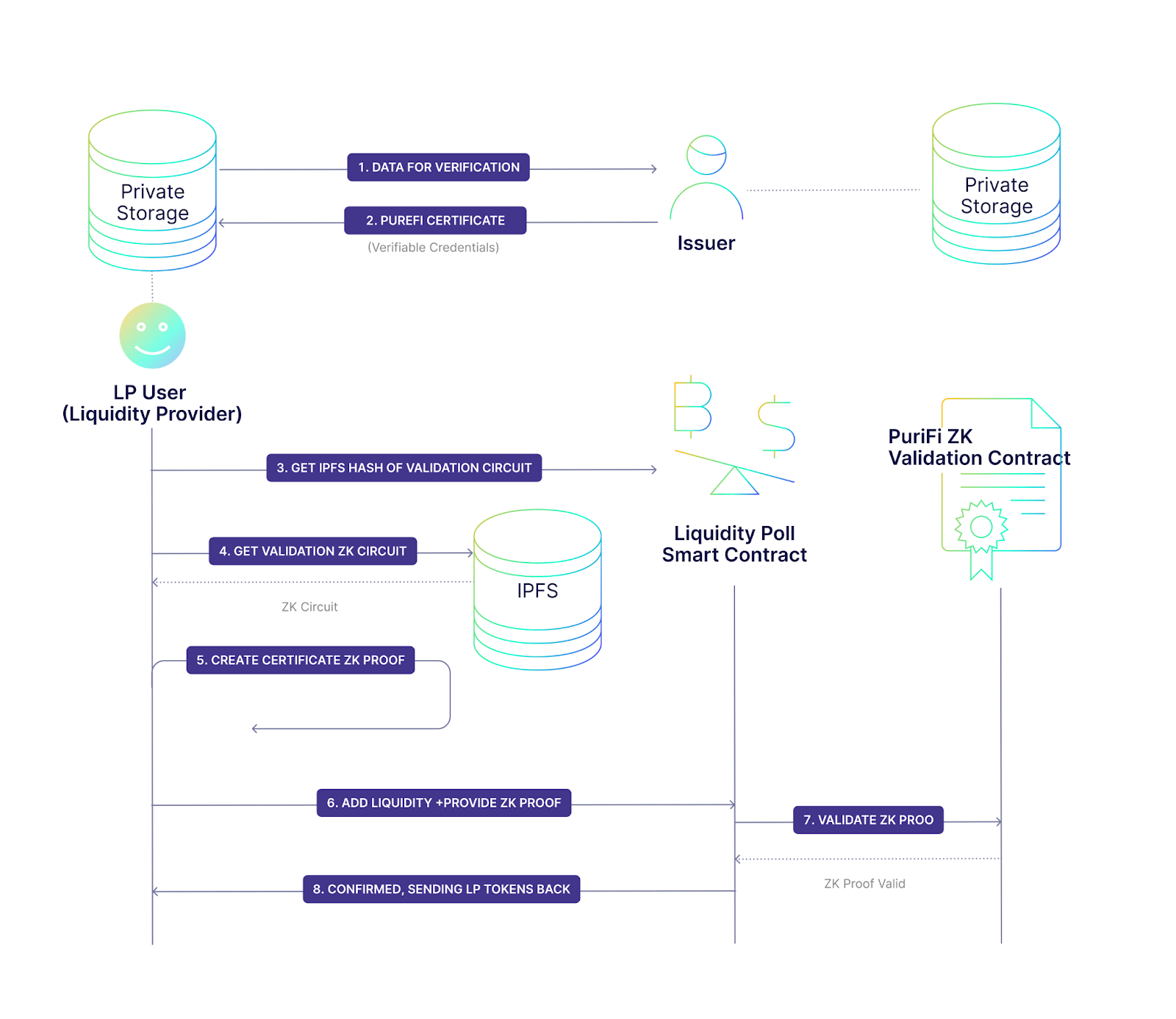

Each Certificate contains information about asset price, AML/KYC and other metadata - so it can be used as a full-fledged AML/KYC verification for any legal/validation purposes. Verifiable Credentials format enables for selective disclosure protocol usage thus enabling credentials holders to security share the minimum required amount of data with validators. PureFi will also utilise a Zero Knowledge based approach to generate secure data proofs capable of being validated with on-chain contracts. This provides users with the unique opportunity of receiving a PureFi Certificate and getting it validated on-chain without any third parties.

How PureFi protocol works

PureFi protocol makes use of 3 general types of users:

- Liquidity Pool Users (LP Users) - users that wish to put their coins into Liquidity Pool and have to prove to Liquidity Pool Operators that their funds are clear.

- Liquidity Pool Operators (LP Operators) - users that control and operate Liquidity Pools, willing to take Liquidity (coins) from LP users, but want to be sure that dirty assets will not pass into their pools.

- Issuers - users (rather companies or enterprises) that are focused on monitoring dirty crypto and can be a trusted party between LP Users and LP Operators that both will rely on when taking decisions within KYC/AML procedures.

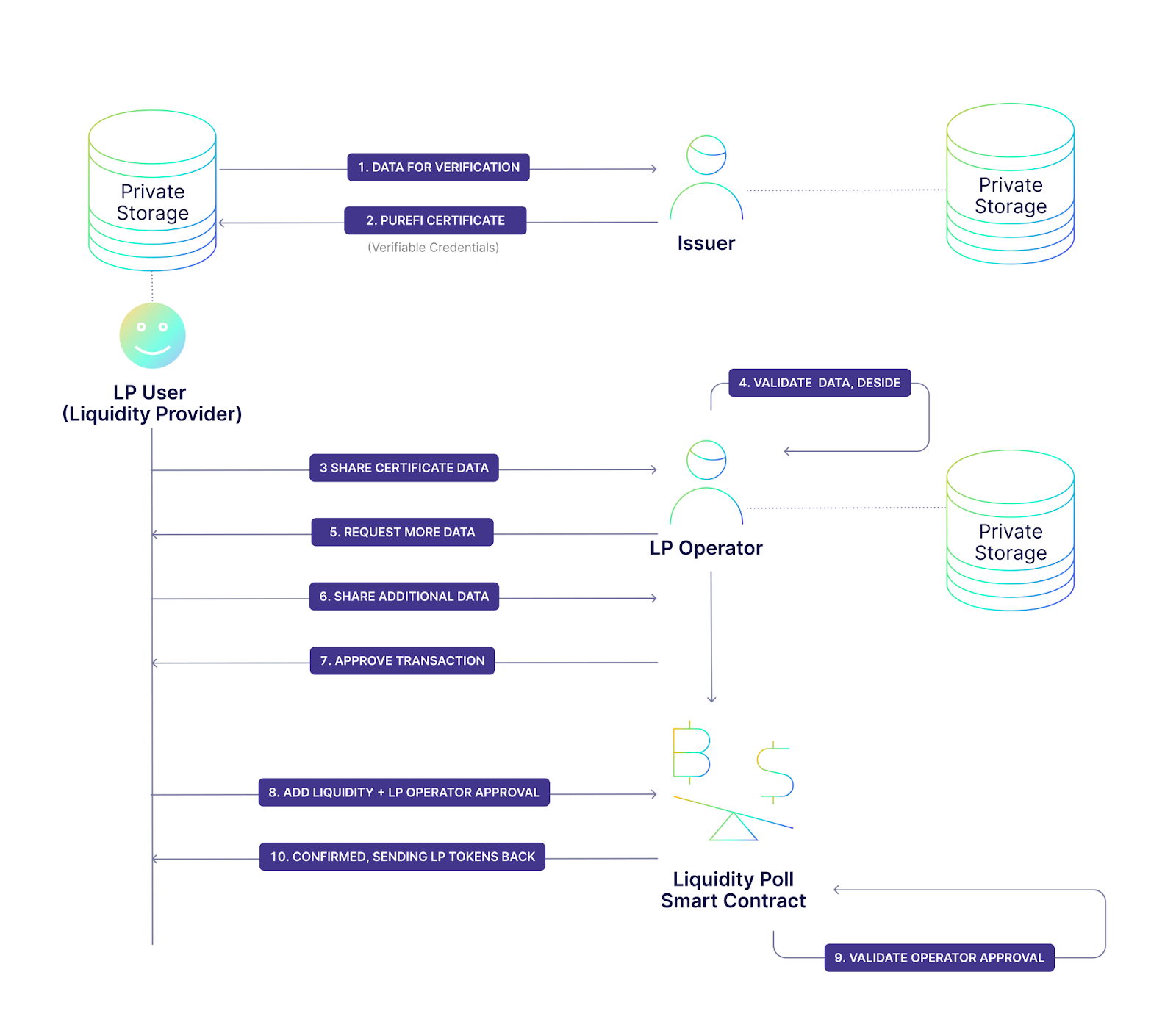

In general, PureFi Protocol makes use of the PureFi Certificates, issued by Issuers to the address of LP Users, and allows LP Operators to build both manual and/or automatic (on-chain) Certificate validation. In case when automatic on-chain validation is applied, Liquidity pool can instantly accept coins and issue LP tokens.

- Liquidity pool user (LP User)

- The LP User specifies the wallet with some balance in crypto that he/she wishes to add as a liquidity into a Liquidity Pool, then sends it to the Issuer.

- The Issuer analyses ML (money laundering) risks and generates the PureFi Certificate in a form of Verifiable Credentials, which includes originating wallet address, coins amount, date and AML risk score.

Result A: If the risk score is higher than the threshold, the protocol will offer to refund money to the sender.

Result B: If the risk score is less than threshold, a VC certificate will be generated from the JSON-file, and the coins will be automatically sent to the liquidity pool smart contract address. The VC certificate can be customized individually. For example, the user may specify personal information and a whitelist of addresses (public key) from which the data can be read. The whitelist can be updated any time.

- LP User is now required to use a PureFi Certificate data to receive an approval for his/her funds to be accepted in the Liquidity pool. This can be done with either of 2 ways:

- By security sharing PureFi Certificate data with the pool Admin via Selective Disclosure protocol based on DID and Verifiable Credentials standards

- Generating a ZK Proof that can be automatically validated by the Smart Contract

- LP User sends funds to Liquidity Pool contract with either Admin approval or ZK Proof. After the Liquidity Pool contract validates the data, it can accept crypto, issue LP tokens and send them back to LP User.

- Liquidity pool operator (LP Operator)

- The liquidity pool (LP) operator may filter liquidity from LP users into his pools in either 2 ways:

- by requesting PureFi Certificate data directly from LP Users in a trusted way via Selective Disclosure protocol. This way not only AML risk score could be shared, but also private data (PII) which could be required by KYC procedures. This approach allows for manual checks and has an LP Admin Approval as final step. Then this Approval will be used by LP User when adding liquidity into the pool.

- by establishing a set of validation rules on the PureFi Certificate data, which could be automatically validated _privately_ by applying Certificate data to ZK Circuit. After data is processed by Circuit, a ZK Proof is generated that cryptographically proves that Certificate data matches the rules established by LP Operator. Then this Proof will be used by LP User when adding liquidity into the pool.

- PureFi Certificate Issuers

- The Certificate Issuers can profit from LP users that will request PureFi Certificates. PureFi protocol relies on the direct data exchange between LP Users and Issuers which allows for maximum flexibility for Issuers to build a secure and trusted service.

- PureFi establishes a set of formal requirements for Issuers to support PureFi protocol features, then whitelists trusted Issuers and maintains Issuers Revocation List.

Tokenomics

PUREFI token (UFI)

PUREFI token (UFI) is the ERC20 token minted on the Ethereum blockchain and Binance Smart Chain (BSC) that empowers the PUREFI protocol. The key utility function of UFI is to provide access to PureFi services, to enable the circulation within PureFi protocol, receive new oracles and protocol updates, as well as enable cryptoasset analytics and identity verification.

Service usage models

There are four levels of service models based on the capacity a client would need PureFi services. In all models PureFi accepts most major cryptocurrencies, UFIs and fiat as a payment.

Basic – occasionally service usage. Basic tariffs.

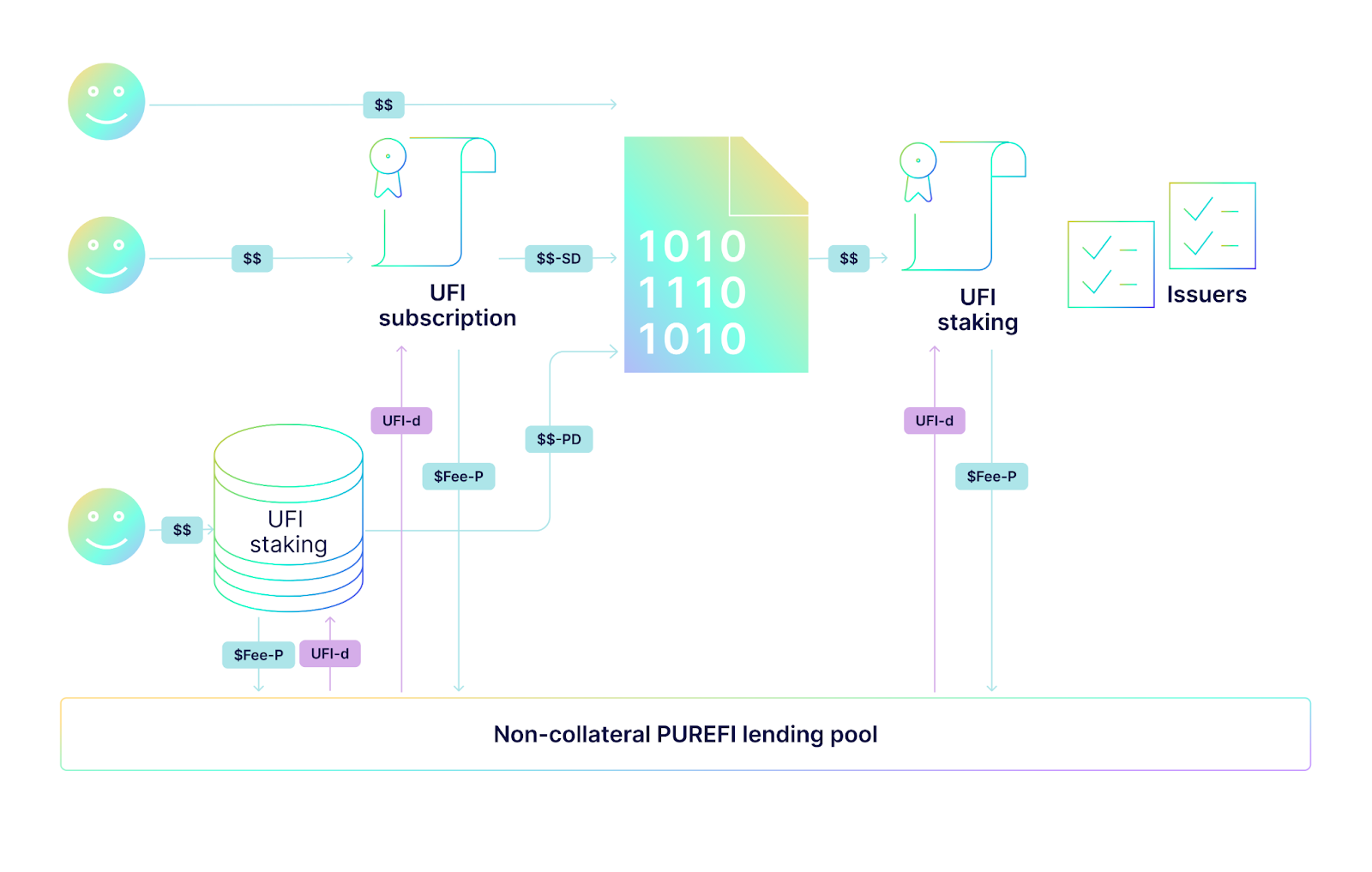

Subscription – more frequent service usage. A user can subscribe for 6 or 12 months service packages and be eligible for the overall subscription discount (SD). The subscription fees are paid in most major cryptocurrencies, UFIs and fiat. A user is issued with an expired and non-tradeable derivative of UFI (UFI-D) associated with a particular service package via Non-collateral PureFi lending protocol.

Professional – big players: DEXs, LPs, funds, protocols, etc. are eligible for the professional packages discount (PD). Pre-conditions – UFIs pooling that also might be borrowed through non-collateral PureFi lending protocol.

Issuer – a compliance provider sorted out and vetted with PureFi standards. There is a pre-condition to be met – UFIs pooling.

Fee-P – the proportion of overall fees distributed to non-collateral PureFi lending protocol.

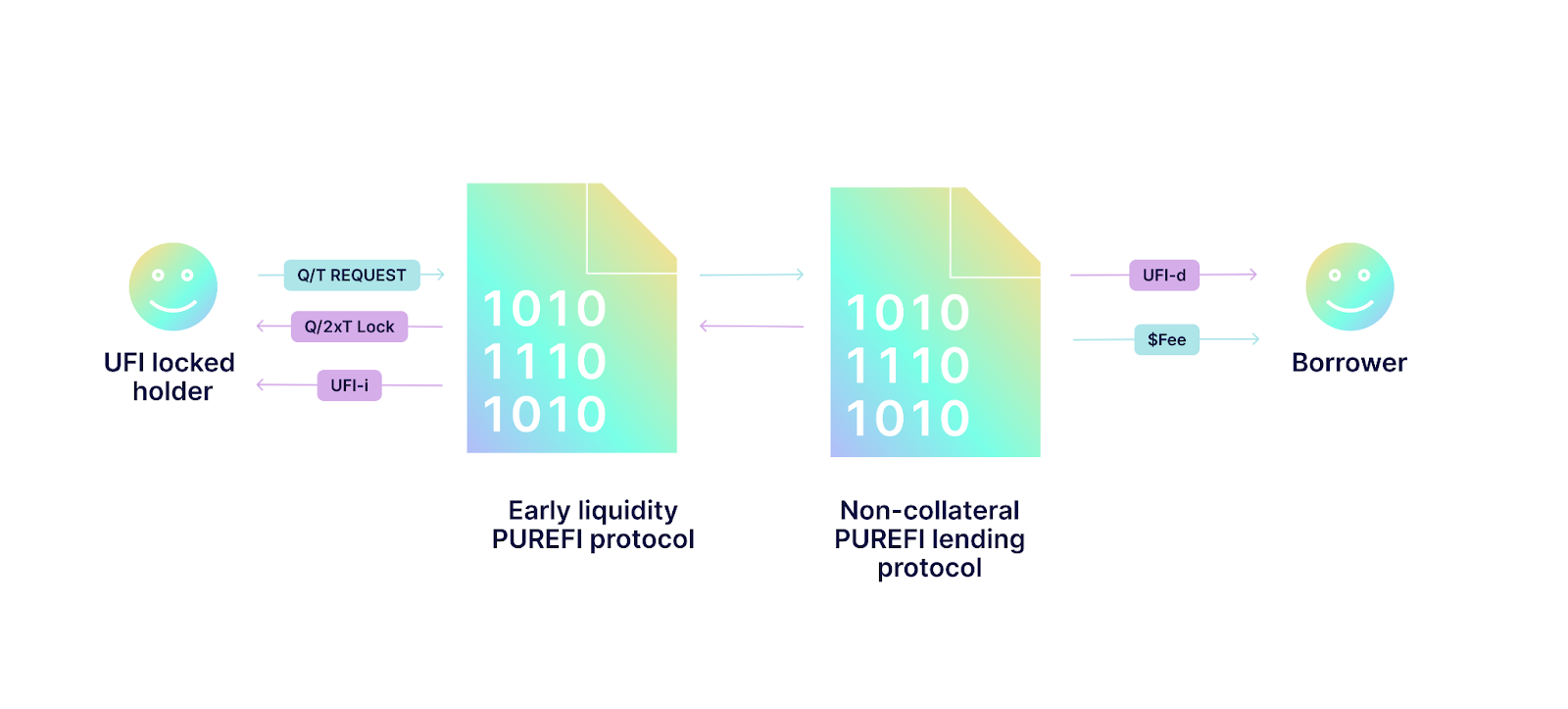

Non-collateral PureFi lending protocol

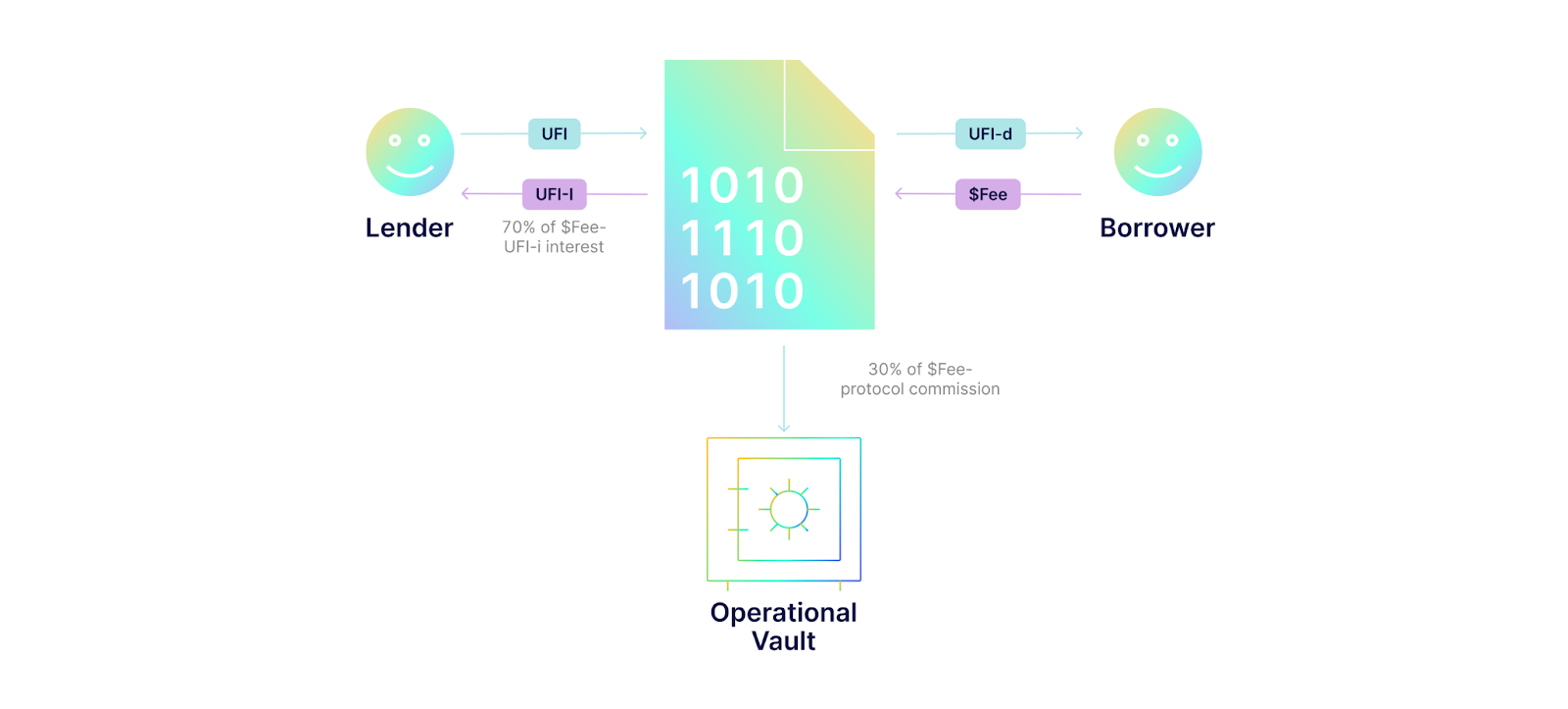

PureFi lending protocol - a pool attached to an audited smart contract to supply extra liquidity to PureFi ecosystems and to give extra incentives to our community:

UFI-i: an interest UFIas proof that a lender has placed UFI into the pool that will be issued as a user lends UFI to the pool and represents a right to earn an interest on their UFI if someone else borrows them.

UFI-d: an expireble and non-tradeable derivative of UFI that will be issued to a borrower based on the length and volume of UFI borrowed.

$Fee - is determined from how much and for how long a borrower would like to lend the UFI and what is the balance between lent and borrowed UFIs in the pool already – the more borrowed the higher the fee.

In the PureFi lending protocol a borrower will have no need for a collateral, and so there is no risk associated with borrowing.

The lender always gets interest in liquid coins paid by the borrowers as fees. They may always withdraw their UFIs if they don't want to participate in fee distribution anymore.

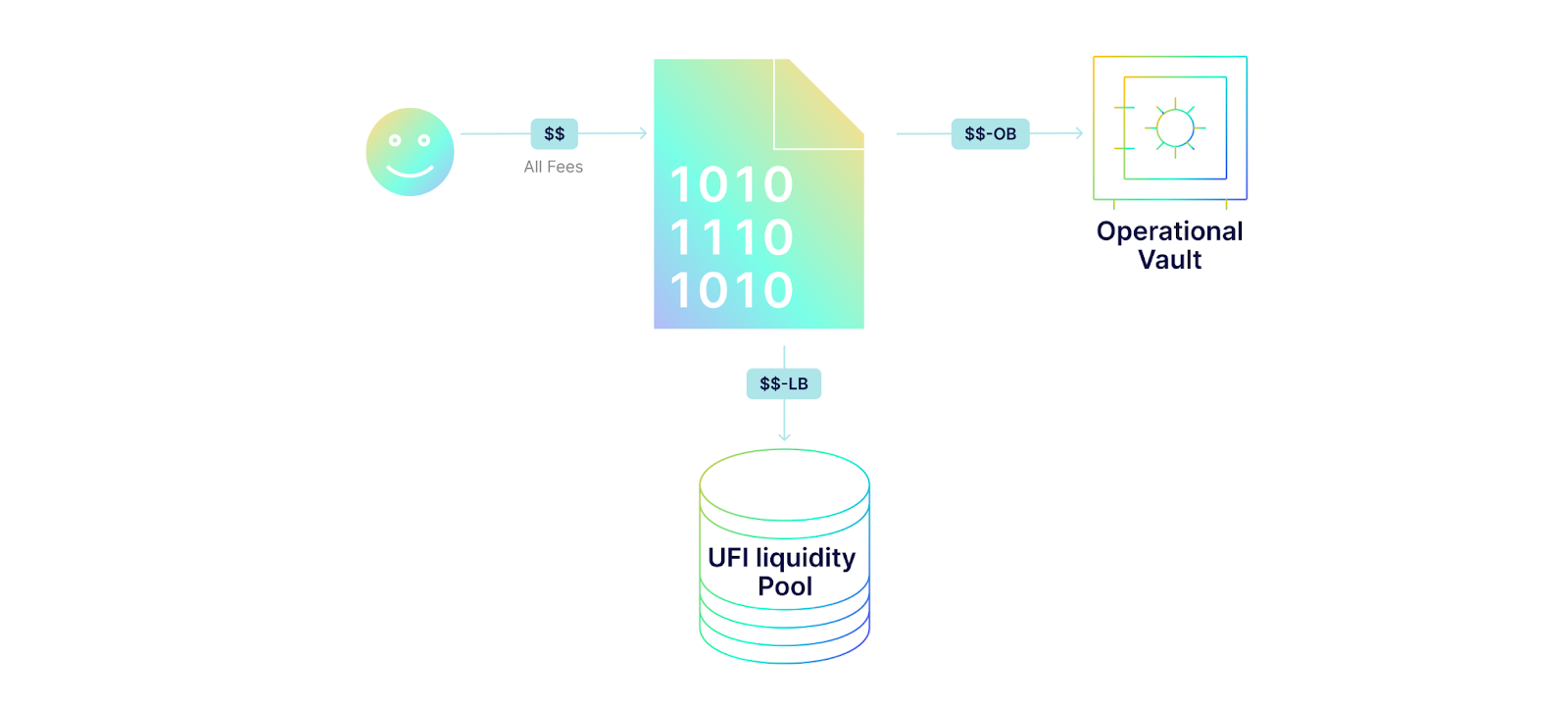

Fees distribution and UFIs Liquidity Pool

All commissions for PureFi protocol are to be split between OV (Operational Vault) and UFI LP (Liquidity Pool).

OV (Operational Vault) funds are to be used to cover operational expenses related to protocol maintenance and infrastructure support.

UFI LP (Liquidity Pool) is a mean of UFI liquidity support and secondary token circulation.

The split or proportion between OV (Operational Vault) and UFI LP (Liquidity Pool) is determined by the balancing coefficient (BC) that accounts the current demand of UFI token: the higher the demand the lower distribution of the fees to UFI LP:

If:

- the maximum price of the UFIin the public round.

- the weekly weighted average price of UFI token in the LP in the preceding week.

All fees are distributed to the UFI LP.

If:

And:

The proportion distributed to OV (Operational Vault):

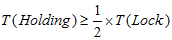

Locked tokens in the early liquidity protocol

PureFi is proud to announce the absolutely new and unique early liquidity protocol for the locked tokens. That protocol gives additional benefits to the early UFIs holders and adds extra liquidity to our ecosystem.

All UFI holders are eligible to join to non-collateral PureFi lending protocol if they meet the following criteria:

1.

2.

- Time of the locked UFIs holding.

- Period of UFIslock.

- Period of UFIsborrowing to the non-collateral PureFi lending protocol.

Q/T Request - UFI holder defines the length and volume of UFIs a user wishes to borrow

Q/2xT Lock - extra locking period added to the previous one for the volume UFI holder is borrowing.

UFI token rounds

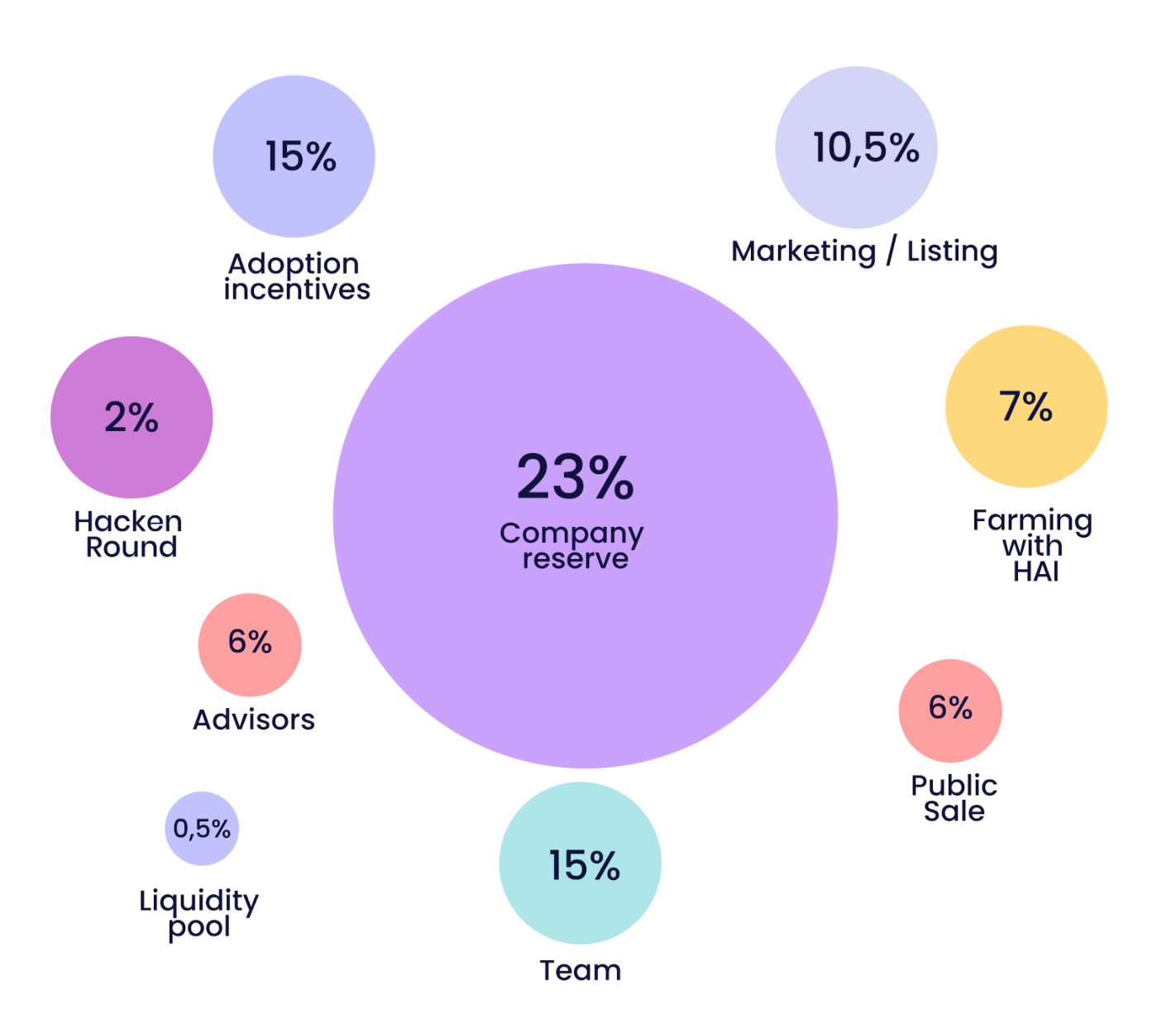

According to UFI’s token model, 100,000,000 UFIs will be minted and distributed within 4 rounds: Privet Round A, Privet Round B, Hacken and Public.

Supply | Total Supply, % | Price per token | USDT to be raised | day 0 unlock | Unlock schedule | Full unlock period | |

Private Round A | 8 000 000 | 8,00% | $0,030 | $ 240 000 | 10,00% | 3 months cliff +10% linear unlock | 12 months |

Private Round B | 7 000 000 | 7,00% | $0,035 | $245 000 | 0,00% | 5 months cliff + 10% linear unlock | 15 months |

Hacken Round | 1 999 500 | 2,00% | $0,040 | $79 980 | 10,00% | 18,00% monthly | 5 months |

Public Sale | 6 666 667 | 6,67% | $0,045 | $300 000 | 33,00% | 33.5% 2nd, 3rd months | 3 months |

Liquidity pool | 500 000 | 0,50% | 0,00% | n/a | n/a | ||

HAI Pool | 7 000 000 | 7,00% | 0,00 | 2 weeks cliff, then linear vesting over 36 months | 36.5 months | ||

Marketing | 10 500 000 | 10,50% | 0,00% | 1 month cliff, then linear vesting over 24 months | 25 months | ||

Team | 15 000 000 | 15,00% | 0,00% | 6 month cliff, then linear vesting over 36 months | 42 months | ||

Adoption incentives | 14 333 333 | 14,33% | 0,00% | n/a | n/a | ||

Advisors | 6 000 000 | 6,00% | 0,00% | 4 month cliff, then linear vesting over 24 months | 28 months | ||

Company reserve | 23 000 000 | 23,00% | 0,00% | 12 months cliff, then linear vesting over 24 months | 36 months | ||

Total | 100 000 000 | 100,00% | |||||

USDT to be raised | 100,00% | $864 980 |

Private Rounds

15,000,000 UFIs at the price of $0,03 (Private A) & $0,035 (Private B) ($485,000) are an extra incentive for the team and founders to fund the project and boost their efforts for its development, also accessible to large investors, such as investment groups or funds, existing cryptocurrency or venture capital investors looking for diversification. The initial unlock schedule equals 10% from the purchase amount for Private Round A and 10% in 5 months for Private Round B. The remaining 90% will be unlocked within 13 months (Private A) and 14 months (Private B).

Hacken round

1,999,500 UFIs at the price of $0,04 ($79,980) will be held specifically for the Hacken community. The initial unlock schedule equals 10% from the purchase amount and the remaining 90% within 5 months.

Public round

6,666,667 UFIs at the price of $0,045 ($300,000) will be available to all small and large investors, and groups and individuals, and focused mostly to expand the PUREFI community. The initial unlock schedule equals 33% from the purchase amount and the remaining 67% within 3 months.

Liquidity pool

500,000 UFIs ($22,500) and the corresponding amount of ETH at the public round price will be locked in the UFIs/ETH pool on Uniswap.

Farming UFIs

7,000,000 UFIs will be farmed via HAI token staking. The accrual system is proportional. The farming system is uniform.

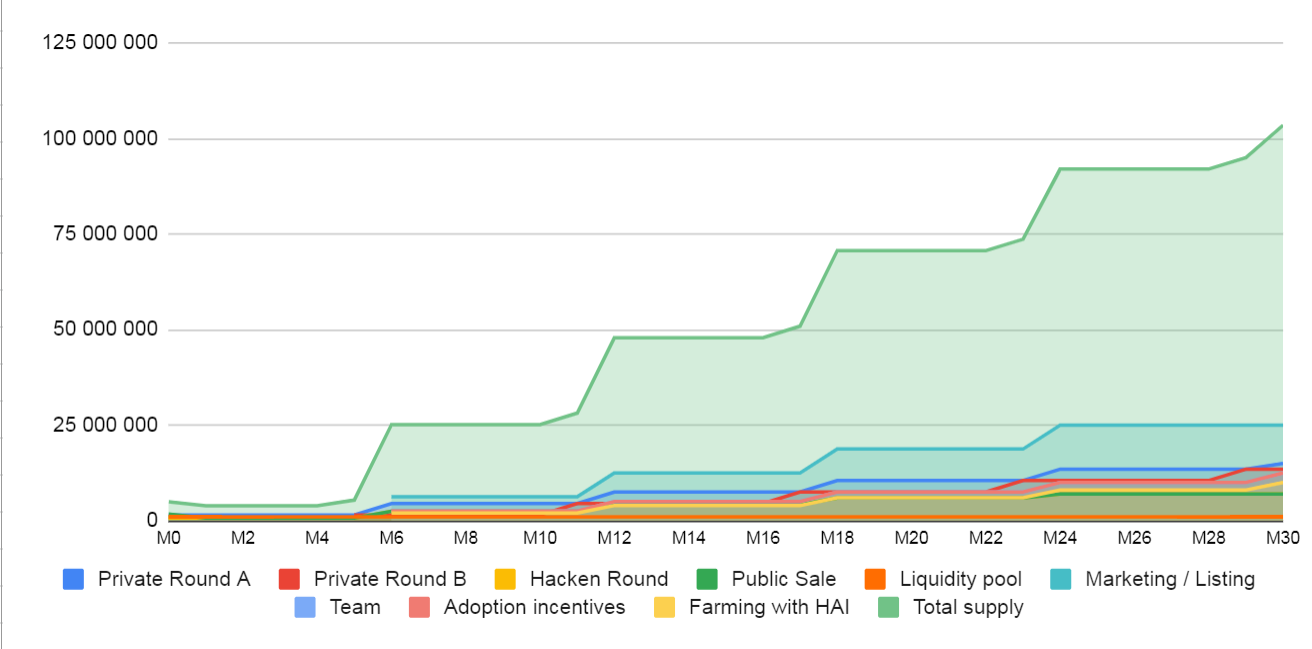

UFIs unlock schedule

The unlocking schedule ensures a gradual UFIs inflows into the circulation capped at 100,000,000 (100 million) throughout its lifetime, thus limiting supply and forming a deflationary token model.

30 months unlocking schedule:

Usecases

Case A: the user supplies liquidity to the unregulated liquidity pool.

PureFi will provide an intermediate smart contract that will stand between the user and the liquidity pool smart contract. The user will have to obtain a Certificate from the Issuer before adding liquidity to the pool. When an intermediate smart contract is triggered, it validates the issued Certificate, checks for the risk factor to be within the defined range, and approves further funds transfer to the liquidity pool. The liquidity tokens are directly transferred to the user’s wallet and never reach an intermediate contract.

Case B: the user supplies liquidity to the regulated liquidity pool.

In case Liquidity pool operators are willing to check for the ML risks (and KYC, optionally) for any crypto deposited into their pool, they may directly integrate a smart contract code that will validate PureFi Certificates. This way the user has to obtain a Certificate upfront and provide this certificate when adding liquidity into the pool. PureFi protocol allows for generating Certificate proofs that allow public pools to validate Certificates without disclosing any private data.

Case C: the liquidity pool operator accepts liquidity from the unknown user.

The liquidity pool operator accepts liquidity from users, then parks this liquidity and triggers the Issuer to provide the transaction hash. Issuer validates incoming crypto and provides the liquidity pool operator with the PureFi Certificate. Based on Certificate data received, the liquidity pool operator may accept the crypto and issue liquidity tokens back, or reject the payment. At any point, the user may withdraw their funds from the parking lot, or get liquidity tokens back.

Case D: The decentralized exchange has regulatory restrictions on user registration (e.g.

DEX does not authorize US residents and users under the age of 18).

First, the user obtains the PureFi Certificate from one of the Issuers. Then, provides information required by the DEX by generating secure PureFi Certificate proof locally, on its device, thus providing the DEX with a cryptographically strong proof (ZK SNARK based) that requested data matches regulation requirements without DEX accessing users private data. In this way, the user remains completely anonymous, and DEX meets the regulatory requirements.

Case E: The tax authority requests information about the origin of users’ funds and the price of crypto assets purchased. Assuming the user obtained the PureFi Certificate from the Issuer when the initial operation was performed (liquidity added into the DEX pool, for example), the user can prove the origin, price, and ML risks taken to the tax authority.

Case F: A law enforcement agency makes a request to the user due to the initiated criminal case in which the dirty money trail led to the user (through the unregulated DeFi). Assuming the user obtained the PureFi Certificate from the Issuer when the initial operation was performed (liquidity added into the DEX pool, for example), the user can prove the origin, price, and ML risks taken to the law enforcement agency.

Roadmap

Q3/2021 Milestone 1 PureFi tokenomics baseline

- Set of lending-borrowing contracts

- $UFI Pool

- $UFI Dex Integration

- Pooling

Q3/2021 Milestone 2 PureFi Protocol

- Verifiable Credentials Standards and document formats for:

- AML

- KYC

- Other Meta Standards

Q4/2021 Milestone 3 Integration with DEXs

- DEX integration KIT

- Circuit

- AML

- KYC

- Other

- ZK-SNARK setup procedure (Public event)

- Intermediate validation contract for EVM compatible blockchains

- Intermediate smart contract for Substrate

- Intermediate smart contract for CosmWasm

Q1/2022 Milestone 4 Issuers SDK

- $UFI pooling

- Onboarding procedure

- External reference API

Total addressable market

On May’2021, the DeFi market value was more than $130 billion (by CoinMarketCap) and increased by nearly 1600% in 7 months. DEX as the most popular DeFi application is extremely interested in the ML/TF debates around the DeFi market. The lack of a KYC procedure in DEX makes it easier for users to trade - just make a new wallet in-app and start trading right now. But on the other hand we are facing the statistically growing risk of ML/TF exactly on DEXs.

For instance, in 2020 the proportion of “bad coins” (e.g. coins coming from or going to: exchange with low score, scam, community reported scam, mixing service, hack and suspicious) on Uniswap was between 0.02% and 2.34%, Kybernetwork and 1Inch - about 1%, and Sushiswap - 0.5%.

However numerous transactions performed between these top-5 DEXs could be defined as low-scored and suspicious: 36.32% of funds on Uniswap going through DEX with bad scores (out of 40.8% funds with bad score), 55.58% on Kybernetwork (out of 55.8%), 57.40% on 1inch (out of 57.6%) and 47.83% on SushiSwap (out of 47.9%). So we can see - the risk of getting “dirty” money trail or falling under money laundering suspicion for the DEX user is quite high and all these transactions could be analysed and evaluated by the PUREFI.

When calculating an approximate DeFi market for the protocol, it is also worth starting from the statistics of illegal transactions on centralized crypto exchanges. According to the CipherTrace’s 2020 Cryptocurrency Crime and Anti-Money Laundering Report, bitcoin addresses with criminal roots sent at least $3.5 billion in bitcoins in 2020, accounting for less than 1% of overall crypto transactions. Summarizing various analyses and assessing the volume of potential illegal actions in the DeFi market, we predict that in 2021 the minimum volume of criminal transactions will be from $1.4 billion.

DeFi AML/KYC regulation analysis & forecasts

And the result is obvious - such an explosion of scams and suspicious activity on DEXs drew more and more attention from the regulators and compliance officers.

We all know that 2020 has been a crypto regulation year since worldwide governments have started to define the regulatory framework mainly in order to comply with the Financial Action Task Force (FATF) recommendations. More control is expected to return to the global crypto industry in 2021/2022. As an example:

- UK: All fintechs with cryptocurrency-related operations should register with the Financial Conduct Authority (FCA); also in the first quarter, the UK's Cryptoasset Task Force will have an update on the potential regulatory consequences of stablecoin adoption.

- Furthermore, FATF intends to release an update on tracking the existing challenges and opportunities associated with the effects of financial innovation by 2021.

(and that includes the cryptomarket as well). - The 6th Anti-Money Laundering Directive came into force in the EU this year.

After all, 2021 will be the year of implementation. Forecasted keypoints:

- It is difficult to see any significant changes in the European regulation on Markets

in Crypto Assets (MiCa) by 2021. Even so, we know that the Commission's working group will be alive and working on the proposed legislation. - In the United States, 2021 will be a significant crypto year, since the STABLE act –

a bill aimed to protect people against potential risks – requires more clarity

and an update.

Legal

This document is provided for your information only and is not meant to be legally binding. UFI token is a utility token, designed for accessing the PureFi services. It is not intended to be a regulated financial product of any kind.

UFI tokens are not intended for sale or use in any jurisdiction where their sale or use is prohibited.

The Initial Token Offering project presented by Avelot Limited is an unregulated fundraising operation. UFI tokens are not securities within the meaning of Hong Kong securities laws. This Whitepaper has not been registered under any securities laws of any country and not meant to generate any form of investment return. This Whitepaper does not constitute an offer or an invitation to sell shares, securities, or rights belonging to Avelot Limited or any related or associated company.

UFI tokens confer no other rights in any form, including but not limited to any ownership, distribution (including but not limited to profit), redemption, liquidation, proprietary (including all forms of intellectual property), or other financial or legal rights, other than those specifically described in this Whitepaper.

Participating in an ITO is a high-risk activity. UFI token purchasers acknowledge and agree that there are risks associated with purchasing, holding, and using UFI tokens in connection with PureFi services, including, without limitation, the risks of capital loss, regulatory risks and market volatility. UFI token purchasers acknowledge, and agree that their decision to purchase, hold and/or use UFI tokens is based solely on the right to potentially use the tokens for PureFi services and not for any expectation of financial gain because of the fluctuations in the value of the tokens.

You should carefully consider the risks, costs, and benefits of acquiring UFI tokens. By participating in this ITO, the purchaser is aware and accepts the risks related to security, the potential lack of technical and economic results, and the total or partial loss of its capital. The purchaser declares being aware of the legal uncertainty of this type of transaction and to have conducted his own legal guidance according to the applicable law.

The ability to utilize PureFi services and UFI token value is not guaranteed. Unforeseen circumstances might not allow the completion of PureFi Protocol development. In such a case, the purchaser expressly acknowledges and accepts that neither Avelot Limited nor its affiliates, directors, shareholders, employees or subcontractors shall be held liable for any direct or indirect losses or damages caused by the non-performance, non-deployment or non-implementation of PureFi Protocol, unavailability of PureFi services, even in cases where its UFI tokens have lost some or all of their value.

The sale of UFI tokens is final and non-refundable.

__

Disclaimer

This Whitepaper has been prepared by PureFi team solely for informational purposes. This information includes certain statements and estimates provided by the Company with respect to the projected future performance of the Company. Such statements, estimates and projections reflect various assumptions by management concerning possible anticipated results, which assumptions may or may not correct. No representations are made as to the accuracy of such statements, estimates or projections.

PureFi makes no representation or warranty as to the accuracy or completeness of this information and shall not have any liability for any representations (expressed or implied) regarding information contained in this presentation. List of risks regarding cryptocurrency can be found here.

PureFi Privacy Policy can be found here.

/